Philadelphia Metro

Metro Area Overview

Market Trend Map

Metro Area Overview

The Home Demand Index (HDI) for the Philadelphia metro area stands at 63 for this report period, up modestly from 61 last month but meaningfully below the 73 recorded during the same period one year ago. The month-over-month gain reflects early seasonal reactivation as buyer attention increases entering spring, though the pace of recovery remains muted relative to prior-year benchmarks. A ten-point year-over-year deficit indicates the Philadelphia market is operating in a softer demand environment than last spring, with affordability pressures and financing sensitivity continuing to constrain buyer engagement across segments.

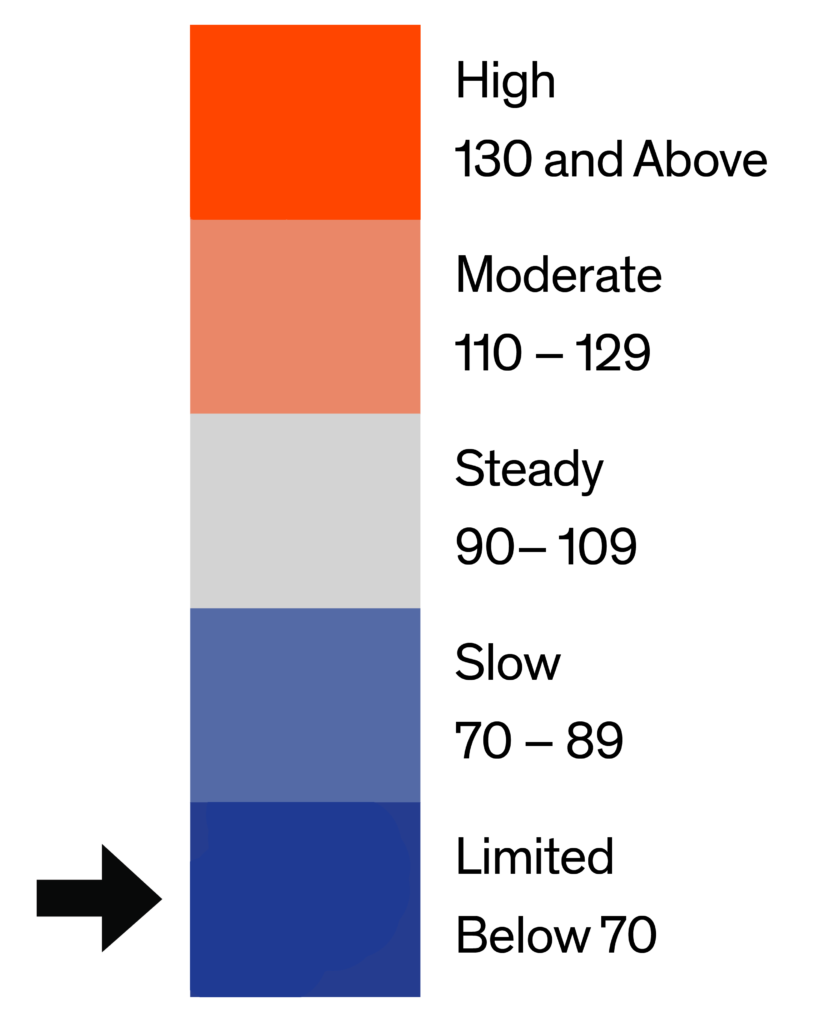

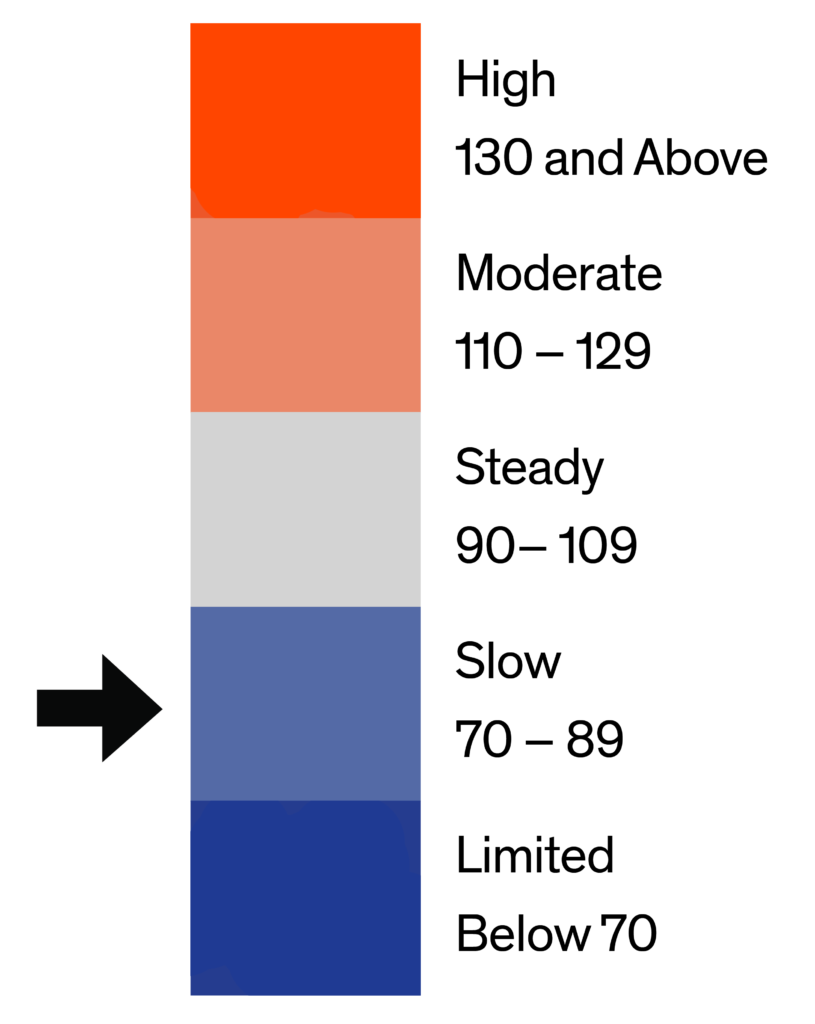

The market trend line, below, provides a high-level monthly overview of the Home Demand Index for each of the metro market areas within the Greater Philadelphia Metro Area. The Home Demand Index is baselined at 100, with 90-110 indicating a steady market. Index values above 110 indicate moderate and high activity while Index values below 90 indicate slower or limited activity. For more information for a given period of time, click on any point on the map to pull up the monthly report.

Metro Market Trend Data by Bright MLS | T3 Home Demand Index

Each of the market areas listed above are defined as follows:

- Central Pennsylvania – Adams, PA; Berks, PA; Cumberland, PA; Dauphin, PA; Franklin, PA; Fulton, PA; Lancaster, PA; Lebanon, PA; Perry, PA; Schuylkill, PA; York, PA;

- Ocean County – Ocean, NJ;

- Philadelphia Metro – Bucks, PA; Burlington, NJ; Camden, NJ; Chester, PA; Delaware, PA; Gloucester, NJ; Kent, DE; Mercer, NJ; Montgomery, PA; New Castle, DE; Philadelphia, PA;

- Salem-Cumberland – Cumberland, NJ; Salem, NJ;

Market Trend Map

The Market Trend Map for the Philadelphia Metro pulls the county map from the monthly reports and combines to provide a time-lapse of the overall market. Use the navigation at the bottom to toggle between months.

Philadelphia Metro County-Level Market Trend Map | Home Demand Index

Current Market Report

Last 6 Market Reports

Historical Market Reports

Data Download

Philadelphia | March 2026

Home Demand Index

The Home Demand Index (HDI) for the Philadelphia metro area stands at 63 for this report period, up modestly from 61 last month but meaningfully below the 73 recorded during the same period one year ago. The month-over-month gain reflects early seasonal reactivation as buyer attention increases entering spring, though the pace of recovery remains muted relative to prior-year benchmarks. A ten-point year-over-year deficit indicates the Philadelphia market is operating in a softer demand environment than last spring, with affordability pressures and financing sensitivity continuing to constrain buyer engagement across segments.

Demand by home type in Philadelphia reflects broad softening relative to last year, though most segments are showing modest month-over-month improvement as the spring season begins. Entry-level single-family homes registered an index of 59, down from 64 last month and below the 73 posted one year ago, indicating that affordability constraints are bearing most heavily on first-time buyers in this market. Mid-range single-family homes edged up to 54 from 53 last month but remain well below last year’s 60, suggesting move-up activity is stabilizing at a subdued level with limited near-term acceleration. Luxury single-family homes posted 39, up from 33 last month but trailing last year’s 51 by a notable margin, pointing to cautious high-end engagement and ongoing hesitancy among discretionary buyers in the upper tier. Entry-level condos advanced to 95 from 88 last month, though they remain below last year’s 99, continuing to represent one of the more resilient demand categories as affordability-focused buyers seek lower-maintenance alternatives. Luxury condos improved to 91 from 82 last month but sit below last year’s 122, reflecting a meaningful year-over-year cooling in premium attached demand that warrants continued monitoring. Townhouses and twin homes rose to 76 from 72 last month, though still below last year’s 87, with the segment’s value proposition sustaining a stable base of buyer interest as spring activity gradually builds.

Monthly Statistics for March 2026

Home Demand

Index

Index

63

(Limited)

Home Demand Index

from prior month

from prior month

61

Home Demand Index

from prior year

from prior year

73

Index change

from prior month

from prior month

3.3%

Index change from

same time last year

same time last year

-13.7%

Bright MLS | T3 Home Demand Index

www.homedemandindex.com

Philadelphia | February 2026

Home Demand Index

The Home Demand Index (HDI) for the Philadelphia metro area is 60 this report period, reflecting a notable increase from 47 last month and signaling a rebound in buyer activity. Compared with the same period last year, when the index stood at 65, demand remains modestly lower on a year-over-year basis. Overall, market conditions point to improving momentum month over month, though activity has not fully returned to last year’s levels.

Demand by home type in Philadelphia shows renewed divergence this report period, with entry-level single-family activity improving modestly while remaining below last year’s levels. Mid-range single-family metrics indicate a sharp rebound from last month, though volatility suggests activity is being driven more by limited inventory than broad-based demand. Overall, buyer engagement remains uneven across segments, reflecting selective purchasing behavior and sensitivity to pricing and availability.

Monthly Statistics for February 2026

Home Demand

Index

Index

60

(Limited)

Home Demand Index

from prior month

from prior month

47

Home Demand Index

from prior year

from prior year

65

Index change

from prior month

from prior month

27.7%

Index change from

same time last year

same time last year

-7.7%

Bright MLS | T3 Home Demand Index

www.homedemandindex.com

Philadelphia | January 2026

Home Demand Index

The Home Demand Index (HDI) for the Philadelphia metro area is 46 in this report period, down sharply from 64 last month and below the 50 reading a year ago. This decline indicates that buyer activity has softened notably, pushing the market further into the Limited demand range after stronger conditions through much of last year. The pullback suggests more cautious buyers and potentially longer selling times, as demand resets to a quieter start-of-year pace.

Demand by home type in Philadelphia continues to show increasing divergence this report period, with notable volatility across single-family segments. Entry-level single-family homes have softened compared with both last month and last year, reflecting ongoing affordability pressures in the most accessible detached segment. Mid-range and luxury single-family homes continue to experience irregular activity, likely driven by limited inventory rather than broad-based buyer interest. Entry-level condos maintain some support, while luxury condos have weakened. Townhouses also remain subdued, reflecting cautious buyer behavior across these segments. Overall, the market continues to reflect uneven demand, with buyers approaching decisions deliberately and selectively.

Monthly Statistics for January 2026

Home Demand

Index

Index

46

(Limited)

Home Demand Index

from prior month

from prior month

64

Home Demand Index

from prior year

from prior year

50

Index change

from prior month

from prior month

-28.1%

Index change from

same time last year

same time last year

-8%

Bright MLS | T3 Home Demand Index

www.homedemandindex.com

Philadelphia | December 2025

Home Demand Index

The Home Demand Index (HDI) for the Philadelphia metro area is 62 this report period, down from 81 last month, signaling a clear month-over-month cooling in buyer activity. Demand is also below last year’s reading of 70, indicating softer conditions on an annual basis. With the index now in a slower range, overall market momentum appears to be easing as buyers remain cautious.

Demand by home type in Philadelphia shows growing divergence this period, led by a meaningful step-down in entry-level single-family activity from last month. Entry-level single-family demand is now lower than both last month and last year, indicating affordability is no longer providing the same level of support as it did earlier in 2025. Mid-range single-family metrics appear highly volatile in the provided data, but the broader pattern suggests a market where move-up demand is softer and increasingly dependent on limited, well-priced inventory. Luxury single-family homes are also seeing weaker demand, while lower-priced condos are slowing and higher-priced condos are holding relatively steadier. Townhomes, rowhouses, and twins continue to experience a moderate slowdown, consistent with broader trends across the market.

Monthly Statistics for December 2025

Home Demand

Index

Index

62

(Limited)

Home Demand Index

from prior month

from prior month

81

Home Demand Index

from prior year

from prior year

70

Index change

from prior month

from prior month

-23.5%

Index change from

same time last year

same time last year

-11.4%

Bright MLS | T3 Home Demand Index

www.homedemandindex.com

Philadelphia | November 2025

Home Demand Index

The Home Demand Index (HDI) for the Philadelphia metro area stands at 80 in the latest report, down from 83 last month. This modest month-over-month decline reflects a continued cooling in buyer activity heading into late fall, consistent with typical seasonal trends. However, compared with last year’s index of 70, overall demand remains stronger year-over-year, suggesting the market is maintaining a healthier pace than in 2024.

Buyer demand across home types in Philadelphia shows a mixed pattern this period. The index for entry-level single-family homes declined to 79 from 85 last month but remains above last year’s 72, suggesting that affordability continues to support first-time buyers. Mid-range single-family homes decreased slightly to 73 from 75, indicating a modest pullback in buyer activity within the mid-tier market, potentially reflecting constrained inventory limiting move-up purchases. Luxury single-family homes declined to 62 from 70 but remain higher than last year, signaling ongoing, though reduced, interest among higher-end buyers. Entry-level condos rose from 106 to 108, up from 77 last year, highlighting strong continued demand among first-time condo buyers. Luxury condos fell to 112 from 120 but remain significantly above last year’s 80, suggesting sustained interest at the upper end of the condo market. Townhouses declined slightly to 88 from 91 last month but remain above last year’s 78, indicating steady demand.

Monthly Statistics for November 2025

Home Demand

Index

Index

80

(Slow)

Home Demand Index

from prior month

from prior month

83

Home Demand Index

from prior year

from prior year

70

Index change

from prior month

from prior month

-3.6%

Index change from

same time last year

same time last year

14.3%

Bright MLS | T3 Home Demand Index

www.homedemandindex.com

Philadelphia | October 2025

Home Demand Index

The Home Demand Index (HDI) for the Philadelphia metro area stands at 82 in the current report, representing a slight increase from 79 last month but unchanged from the same period last year. This modest month-over-month uptick suggests a stabilizing trend in buyer activity, potentially reflecting the typical post-summer market rebalancing. While demand levels are not accelerating, they remain consistent with last year’s pace, indicating that the broader market is holding steady despite ongoing affordability pressures and inventory limitations.

Buyer demand across home types in Philadelphia shows mixed results this period. The index for entry-level single-family homes edged down slightly to 81 from 83 last month but remains above last year’s 81, indicating sustained though slow activity in the more affordable tier. Mid-range single-family homes recorded 74, down from 73 last month and just below last year’s 75, suggesting modest softening as affordability pressures temper move-up buyer activity. Luxury single-family homes rose to 68 from 58 but remain below last year’s 74, while entry-level condos climbed to 104 from 99, and luxury condos jumped to 121 from 104, both above last year. Townhouses increased slightly to 90 from 86, matching last year’s level. Overall, demand is steady but cautious, with stronger activity in condos and luxury segments.

Monthly Statistics for October 2025

Home Demand

Index

Index

82

(Slow)

Home Demand Index

from prior month

from prior month

79

Home Demand Index

from prior year

from prior year

82

Index change

from prior month

from prior month

3.8%

Index change from

same time last year

same time last year

0%

Bright MLS | T3 Home Demand Index

www.homedemandindex.com

Philadelphia | September 2025

Home Demand Index

The Home Demand Index (HDI) for the Philadelphia metro area declined to 77 in the current report, down from 85 last month and slightly below the 81 recorded during the same period last year. This continued month-over-month softening suggests a seasonal cooling in buyer activity as the market transitions from summer into early fall. The year-over-year dip, though modest, points to slightly weaker demand conditions compared to last September, indicating a cautious buyer environment.

Buyer demand across most home segments in Philadelphia declined this period, though levels remain above last year in several categories. The index for entry-level single-family homes edged down from 83 to 81 but stayed higher than the 77 recorded last year, reflecting sustained slow interest. Meanwhile, mid-range single-family homes experienced a sharper pullback, with the index falling to 72 from 80 and below last year’s 78, suggesting affordability pressures are beginning to weigh more heavily in this tier. While some segments remain resilient, the overall market is showing signs of cooling amid ongoing inventory constraints and seasonal transition.

Monthly Statistics for September 2025

Home Demand

Index

Index

77

(Slow)

Home Demand Index

from prior month

from prior month

85

Home Demand Index

from prior year

from prior year

81

Index change

from prior month

from prior month

-9.4%

Index change from

same time last year

same time last year

-4.9%

Bright MLS | T3 Home Demand Index

www.homedemandindex.com

All reports for the Philadelphia Market Area.

List of available data files. Note that the data file includes all data for the report period across the entire Bright MLS footprint.