Baltimore Metro

Metro Area Overview

Market Trend Map

Metro Area Overview

The Home Demand Index (HDI) for the Baltimore metro area stands at 84 for this report period, up four points from 80 last month and below the 96 recorded during the same period one year ago. The four-point month-over-month gain is a counter-seasonal result, July typically marks a deceleration from the June peak as the active selling window narrows, and suggests that a cohort of buyers motivated by the brief rate-dip window that opened during May and June closed transactions into early July, extending the demand signal one period beyond the seasonal ceiling that most years arrives in June. The twelve-point year-over-year deficit, while meaningful, should be read against the unusually strong July 2025 baseline, when the Baltimore metro was completing an extended spring cycle that had been supported by regional employment stability and a temporary easing in rate-lock psychology; the absolute level of 84 reflects a functioning Slow-territory summer market rather than a structural deterioration in demand fundamentals. The widening spread between the condo tiers, which are running at Steady and Moderate levels, and the entry single-family tier, which remains in Limited territory at 62, continues to define the most important cross-segment dynamic in this market, as buyers facing persistent affordability friction at the lowest detached price points migrate into the attached inventory that offers more accessible entry thresholds in a market where financing sensitivity remains the primary demand governor.

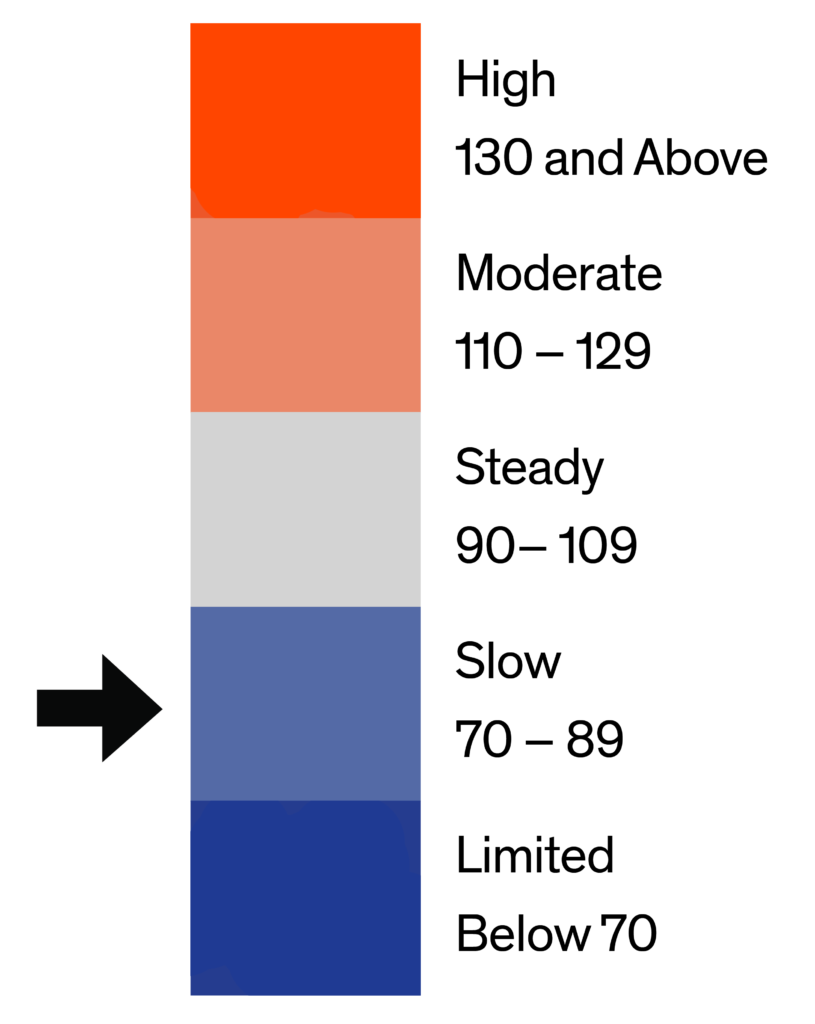

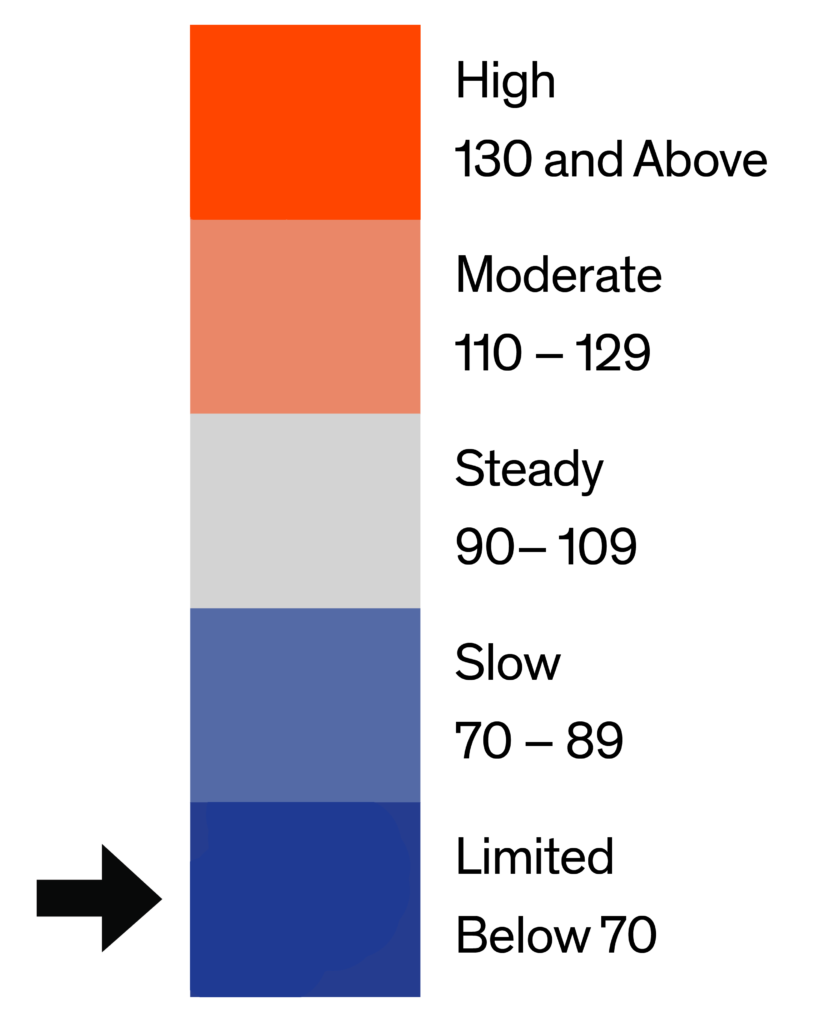

The market trend line, below, provides a high-level monthly overview of the Home Demand Index for each of the metro market areas within the Greater Baltimore Metro Area. The Home Demand Index is baselined at 100, with 90-110 indicating a steady market. Index values above 110 indicate moderate and high activity while Index values below 90 indicate slower or limited activity. For more information for a given period of time, click on any point on the map to pull up the monthly report.

Metro Market Trend Data by Bright MLS | T3 Home Demand Index

Each of the market areas listed above are defined as follows:

- Baltimore Metro – Anne Arundel, MD; Baltimore City, MD; Baltimore, MD; Carroll, MD; Harford, MD; Howard, MD;

- DelMar Coastal – Somerset, MD; Sussex, DE; Wicomico, MD; Worcester, MD;

- Maryland Eastern Shore – Caroline, MD; Cecil, MD; Dorchester, MD; Kent, MD; Queen Annes, MD; Talbot, MD;

Market Trend Map

The Market Trend Map for the Baltimore Metro pulls the county map from the monthly reports and combines to provide a time-lapse of the overall market. Use the navigation at the bottom to toggle between months.

Baltimore Metro County-Level Market Trend Map | Home Demand Index

Current Market Report

Last 6 Market Reports

Historical Market Reports

Data Download

Baltimore | July 2026

Home Demand Index

The Home Demand Index (HDI) for the Baltimore metro area stands at 84 for this report period, up four points from 80 last month and below the 96 recorded during the same period one year ago. The four-point month-over-month gain is a counter-seasonal result, July typically marks a deceleration from the June peak as the active selling window narrows, and suggests that a cohort of buyers motivated by the brief rate-dip window that opened during May and June closed transactions into early July, extending the demand signal one period beyond the seasonal ceiling that most years arrives in June. The twelve-point year-over-year deficit, while meaningful, should be read against the unusually strong July 2025 baseline, when the Baltimore metro was completing an extended spring cycle that had been supported by regional employment stability and a temporary easing in rate-lock psychology; the absolute level of 84 reflects a functioning Slow-territory summer market rather than a structural deterioration in demand fundamentals. The widening spread between the condo tiers, which are running at Steady and Moderate levels, and the entry single-family tier, which remains in Limited territory at 62, continues to define the most important cross-segment dynamic in this market, as buyers facing persistent affordability friction at the lowest detached price points migrate into the attached inventory that offers more accessible entry thresholds in a market where financing sensitivity remains the primary demand governor.

Demand by home type in Baltimore shows a divergent pattern this period that stands in contrast to the broad-based softening observed in the previous period, with the metro-wide counter-seasonal recovery to 84 driven primarily by strength in the attached and upper-tier segments while the entry single-family floor remains constrained. The most notable development across the tier structure is the surge in entry condo demand to 110, a twenty-point month-over-month gain from the previous reading of 90 that represents the largest single-tier sequential move in the current reporting cycle and has pushed this segment into Steady territory for the first time in recent periods. Luxury condos at 124, a ten-point gain from 114 last month, reinforced this signal with a Moderate-range reading that is the highest absolute index across any tier in the metro. Luxury single-family homes at 108 declined three points from 111 last month but remain in Steady territory, while mid single-family held flat at 81 and entry single-family ticked up one point to 62, the latter remaining in Limited territory and continuing to reflect the most acute affordability compression in the metro at the sub-$375,000 detached price point. The townhouse, rowhouse, and twin home segment gained seven points to 87, a Slow-territory reading consistent with the metro average and suggesting that the attached single-family category is contributing meaningfully to the counter-seasonal demand signal alongside the condo tiers. The emerging divergence between a strong attached market and a constrained entry SF market is the defining structural dynamic in Baltimore’s current demand picture.

Monthly Statistics for July 2026

Home Demand

Index

Index

84

(Slow)

Home Demand Index

from prior month

from prior month

80

Home Demand Index

from prior year

from prior year

96

Index change

from prior month

from prior month

5.0%

Index change from

same time last year

same time last year

-12.5%

Bright MLS | T3 Home Demand Index

www.homedemandindex.com

Baltimore | June 2026

Home Demand Index

The Home Demand Index (HDI) for the Baltimore metro area stands at 77 for this report period, down from 93 last month and below the 99 recorded during the same period one year ago. The sixteen-point month-over-month decline marks a pronounced reversal from the spring reactivation that had been building since February, signaling that peak-season demand has rolled over more sharply than seasonal norms would suggest and raising the possibility that affordability constraints and financing sensitivity are reasserting pressure as buyer urgency fades entering the early summer period. The twenty-two-point year-over-year deficit represents the widest annual gap recorded in recent reporting cycles for this metro, indicating that the Baltimore market is now tracking at a measurably softer level than the same period last year, with the structural headwinds of elevated home prices and persistent rate sensitivity continuing to erode the demand base that briefly appeared to be consolidating through the spring.

Demand by home type in Baltimore shows broad-based softening this period, consistent with the metro-wide index declining to 77 from 93 last month, with all segments likely registering meaningful month-over-month retreats as the post-spring demand rollover takes hold across the buyer spectrum. Entry-level single-family homes remain the most constrained tier, with first-time and value-driven buyers continuing to face acute affordability barriers at the lowest price points in a market where financing sensitivity is most pronounced, and the pullback in overall engagement is likely deepest in this segment given the lowest index reading. Mid-range single-family demand is retreating from spring highs as move-up buyer urgency fades, consistent with the market transitioning from the peak-urgency phase of the selling season toward a more measured early-summer pace. Luxury single-family activity, while retreating from its strong May reading, is likely exhibiting greater relative resilience than lower tiers, as discretionary buyers with less financing dependency maintain selective engagement with premium inventory. Entry-level condos continue to meaningfully outperform entry-level and mid-range single-family categories on an absolute basis, maintaining their structural role as the primary affordability outlet in the metro, though they remain below luxury single-family levels. Luxury condos and townhouses, rowhouses, and twin homes are moderating from their spring peaks in line with the broader market, with luxury condos retaining above-metro-average readings, while townhouses, rowhouses, and twin homes are now broadly in line with the metro average.

Monthly Statistics for June 2026

Home Demand

Index

Index

77

(Slow)

Home Demand Index

from prior month

from prior month

93

Home Demand Index

from prior year

from prior year

99

Index change

from prior month

from prior month

-17.2%

Index change from

same time last year

same time last year

-22.2%

Bright MLS | T3 Home Demand Index

www.homedemandindex.com

Baltimore | May 2026

Home Demand Index

The Home Demand Index (HDI) for the Baltimore metro area stands at 89 for this report period, unchanged from 89 last month and below the 98 recorded during the same period one year ago. The flat month-over-month reading signals that the spring reactivation has plateaued rather than continued to build momentum into peak selling season, marking a notable shift from the sequential gains that characterized the recovery through March and April. The nine-point year-over-year deficit indicates the Baltimore market has not yet closed the gap with the prior-year level, with affordability constraints and financing sensitivity continuing to temper buyer engagement even as the market operates near its seasonal peak.

Entry-level single-family activity remains the most constrained tier, with first-time buyers continuing to navigate persistent affordability barriers at the lowest price points in a market where financing sensitivity is most acute, while mid-range single-family homes are tracking at 88, up from 83 last month, as move-up activity sustains without further spring acceleration. Luxury single-family demand remains selective but has rebounded sharply to 115 from 89, reflecting measured engagement consistent with the discretionary nature of this tier and the year-over-year shortfall observed throughout the spring cycle. Entry-level condos continue to outperform detached categories on an absolute basis, consistent with their role as the primary affordability alternative in the metro, while luxury condos, which declined to 135 from 154 last month, may be moderating from elevated readings as the season matures and initial demand absorbs available premium inventory. Townhouses and rowhouses are tracking near 91, down from 97 previously, sustained by their appeal among buyers seeking space-to-price efficiency in a market where detached single-family affordability remains structurally strained.

Monthly Statistics for May 2026

Home Demand

Index

Index

89

(Slow)

Home Demand Index

from prior month

from prior month

89

Home Demand Index

from prior year

from prior year

98

Index change

from prior month

from prior month

0.0%

Index change from

same time last year

same time last year

-9.2%

Bright MLS | T3 Home Demand Index

www.homedemandindex.com

Baltimore | April 2026

Home Demand Index

The Home Demand Index (HDI) for the Baltimore metro area stands at 86 for this report period, up notably from 76 last month but below the 93 recorded during the same period one year ago. This meaningful month-over-month acceleration signals a decisive spring reactivation in buyer engagement, consistent with Baltimore’s historical pattern of demand strengthening through April as seasonal inventory and buyer urgency converge. Despite the annual shortfall, the rebound suggests improving momentum, indicating that the affordability and rate headwinds that suppressed activity through the winter are beginning to ease as conditions stabilize.

Demand by home type in Baltimore shows broad-based improvement this period, with most segments posting meaningful month-over-month gains as spring buyer activity accelerates, though all segments remain below year-ago levels. Entry-level single-family homes registered an index of 71, up from 69 last month and below the 76 posted one year ago, reflecting improving first-time buyer engagement though affordability constraints continue to cap the pace of recovery in this rate-sensitive tier. Mid-range single-family homes advanced to 80 from 67 last month, but remain below last year’s reading of 88, suggesting move-up buyer activity is building meaningful spring momentum after a subdued winter. Luxury single-family homes climbed to 84 from 70 last month, but remain below last year’s 104, pointing to selective but expanding high-end engagement as spring inventory enters the market. Entry-level condos rose to 116 from 110 last month, but remain below last year’s 136, reinforcing their position as the most consistently active demand tier in the metro and a primary affordability alternative for buyers navigating constrained detached home budgets. Luxury condos advanced to 149 from 114 last month, though still trailing last year’s 160, as the high-end attached segment continues to normalize following an elevated prior-spring period that may have pulled forward activity. Townhouses, rowhouses, and twin homes rose strongly to 94 from 85 last month, slightly below last year’s 98, signaling that this segment is nearing prior-spring demand levels and is benefiting robustly from spring buyer reactivation.

Monthly Statistics for April 2026

Home Demand

Index

Index

86

(Slow)

Home Demand Index

from prior month

from prior month

76

Home Demand Index

from prior year

from prior year

93

Index change

from prior month

from prior month

13.2%

Index change from

same time last year

same time last year

-7.5%

Bright MLS | T3 Home Demand Index

www.homedemandindex.com

Baltimore | March 2026

Home Demand Index

The Home Demand Index (HDI) for the Baltimore metro area stands at 73 for this report period, up modestly from 71 last month but below the 80 recorded during the same period one year ago. This month-over-month improvement signals a tentative early-spring uptick in buyer engagement, consistent with seasonal reactivation following the winter slowdown. The year-over-year gap, however, indicates the market has not yet recovered to last March’s demand level, with affordability constraints and rate sensitivity continuing to temper the pace of recovery.

Demand by home type in Baltimore shows a mixed but generally firming picture this period, with most segments holding steady or improving modestly from last month while trailing year-ago levels. Entry-level single-family homes registered an index of 65, down slightly from 66 last month and meaningfully below the 73 posted one year ago, reflecting persistent affordability pressure on first-time and value-driven buyers in the most rate-sensitive segment. Mid-range single-family homes held flat at 65 ‚ unchanged from last month but below last year’s 72‚ suggesting move-up buyer activity has stabilized but not yet accelerated into spring. Luxury single-family homes improved to 66 from 60 last month, though demand remains below the 69 recorded a year ago, pointing to selective high-end engagement rather than broad-based momentum. Entry-level condos continue to outperform detached categories, rising to 105 from 102 last month, though slightly below last year’s 110, reinforcing their role as an affordability alternative for buyers navigating constrained budgets. Luxury condos posted 113, essentially unchanged from 114 last month but notably below last year’s 162, signaling a meaningful year-over-year cooling in high-end attached demand. Townhouses, rowhouses, and twin homes advanced to 82 from 78 last month, though still trailing the 89 recorded a year ago ‚ a segment that continues to benefit from its price-to-space value proposition as spring buyer activity builds.

Monthly Statistics for March 2026

Home Demand

Index

Index

73

(Slow)

Home Demand Index

from prior month

from prior month

71

Home Demand Index

from prior year

from prior year

80

Index change

from prior month

from prior month

2.8%

Index change from

same time last year

same time last year

-8.8%

Bright MLS | T3 Home Demand Index

www.homedemandindex.com

Baltimore | February 2026

Home Demand Index

The Home Demand Index (HDI) for the Baltimore metro area reflects a modest improvement this report period, rising from last month and returning to parity with the same time last year. This rebound suggests buyer activity has stabilized after a softer prior reading, though overall demand remains measured rather than expansive. The combination of month-over-month recovery and flat year-over-year performance points to cautious engagement, with affordability and financing conditions continuing to shape buyer behavior.

Demand by home type in Baltimore shows broad moderation consistent with the overall market, though performance varies by segment. Entry-level single-family homes remain the most constrained, as affordability pressures continue to limit first-time buyer activity. Mid-range single-family homes are comparatively steadier, supported by selective move-up demand. Luxury single-family homes show softer near-term momentum, though underlying interest remains healthier than lower tiers. Entry-level condos continue to function as an affordability alternative, while luxury condos retain relative strength tied to lifestyle-driven buyers. Townhouses, rowhouses, and twin homes show modest year-over-year softness but have gained momentum recently, remaining supported by their balance of price and space.

Monthly Statistics for February 2026

Home Demand

Index

Index

69

(Limited)

Home Demand Index

from prior month

from prior month

56

Home Demand Index

from prior year

from prior year

69

Index change

from prior month

from prior month

23.2%

Index change from

same time last year

same time last year

0%

Bright MLS | T3 Home Demand Index

www.homedemandindex.com

Baltimore | January 2026

Home Demand Index

The Home Demand Index (HDI) for the Baltimore metro area stands at 55 in this report period, down from 73 last month and slightly below the 57 reading recorded one year ago. This latest move reinforces that the market is operating in a subdued demand environment, with buyer activity clearly weaker than both recent and prior-year benchmarks. The combination of a sharp month‑over‑month decline and a modest year‑over‑year shortfall points to affordability pressures and rate sensitivity weighing on purchasing decisions, with more households delaying moves or narrowing their search criteria.

The comparative chart for Baltimore shows that the decline in the overall Home Demand Index to 55 is being felt across all home types, with demand generally cooler than in recent periods but not uniformly weak. Entry-level single-family homes remain under the greatest pressure as first-time and value-oriented buyers confront tighter affordability and limited listings, while mid-range single-family homes show moderating but comparatively more resilient activity from established move-up households. Luxury single-family demand has also eased from prior highs, yet affluent buyers and cash purchasers continue to provide a measure of support that keeps this tier healthier than the entry segment. On the attached side, entry-level condos and luxury condos still tend to outperform detached product, with the former serving as an affordability alternative and the latter benefiting from lifestyle and amenity-driven demand, even if both have softened from earlier peaks. Townhouses, rowhouses, and twin homes show mild cooling consistent with the broader market, but their price-to-space value proposition and desirable locations help maintain a stable base of interest.

Monthly Statistics for January 2026

Home Demand

Index

Index

55

(Limited)

Home Demand Index

from prior month

from prior month

73

Home Demand Index

from prior year

from prior year

57

Index change

from prior month

from prior month

-24.7%

Index change from

same time last year

same time last year

-3.5%

Bright MLS | T3 Home Demand Index

www.homedemandindex.com

All reports for the Baltimore Market Area.

List of available data files. Note that the data file includes all data for the report period across the entire Bright MLS footprint.